facilitate the formation of banks whose functions should principally, if

not exclusively, consist in the financing of industrial undertakings. No

such bank, however, has been started, a fact that is probably due to the

very rigorous terms prescribed by the Act respecting these banks, more

especially the item that only banks were entitled to be shareholders in an

Underwriting Bank. The difficulty has been practically obviated by

ordinary companies being formed to finance industrial enterprises, such

companies being governed of course by the laws affecting limited liability

companies. Such banks as are entitled to possess shares can then become

shareholders in any such company. Among the companies of this type

the best known are: Svenska Emissionsaktiebolaget, Aktiebolaget Provi-

dentia, Aktiebolaget Svenska Emissionsinstitutet, and Einansaktiebolaget.

The principal activity of the banks consists in making advances for short

periods with the money deposited with them by the public. The different

forms of deposit business are as follows: a) Deposit Accounts, under two

headings, depositionsrakning and kapitalrakning, the difference between

which is only of a formal kind, for sums that are to be repaid at a given

date or stated notice; b) Accounts Current or Cheque Accounts, for money

to be repaid at call; and c) Savings-Bank Accounts, for money deposited

on conditions which are practically the same as those in force for Savings-

Banks.

Advances are usually made in one of the three following ways: a) The

discounting of bills; b) the granting of loans on the security of mortgages,

debentures, stocks, and shares, etc., or on personal guarantee; c) the allowing

of overdrafts or cash credits ofl similar security. Another form of

account is the running account, practically a combination of cheque

account and cash credit, enabling the customer, in accordance with

agreement and on security lodged, to overdraw his account at the bank up

to a stipulated amount.

The various articles of association of the banking companies, which

have been duly authorized by the Government, embrace a prohibition

for the several banks to discount bills or to accord loans for a longer space

of time than six months, or to grant the right to overdraw an account for

more than one year. Some banks, however, are also entitled, subject to

certain restrictions, to grant loans repayable by instalments for at most

ten years. The several articles of association likewise contain a prohibition

on banks granting credit on the security of only one g u a r a n t o r s

name.

The banks carry on besides a number of other branches of activity-

Thus, they issue hank post hills (generally speaking sight drafts drawn

on some Stockholm bank, which according to mutual agreement among

the banks are cashable at any banking establishment throughout the

country); they also issue letters of credit to travellers, payable at any of

the more important towns on the continent, undertake the collecting of

matured hills, dividend warrants, drawn bonds etc:, accept securities depo-

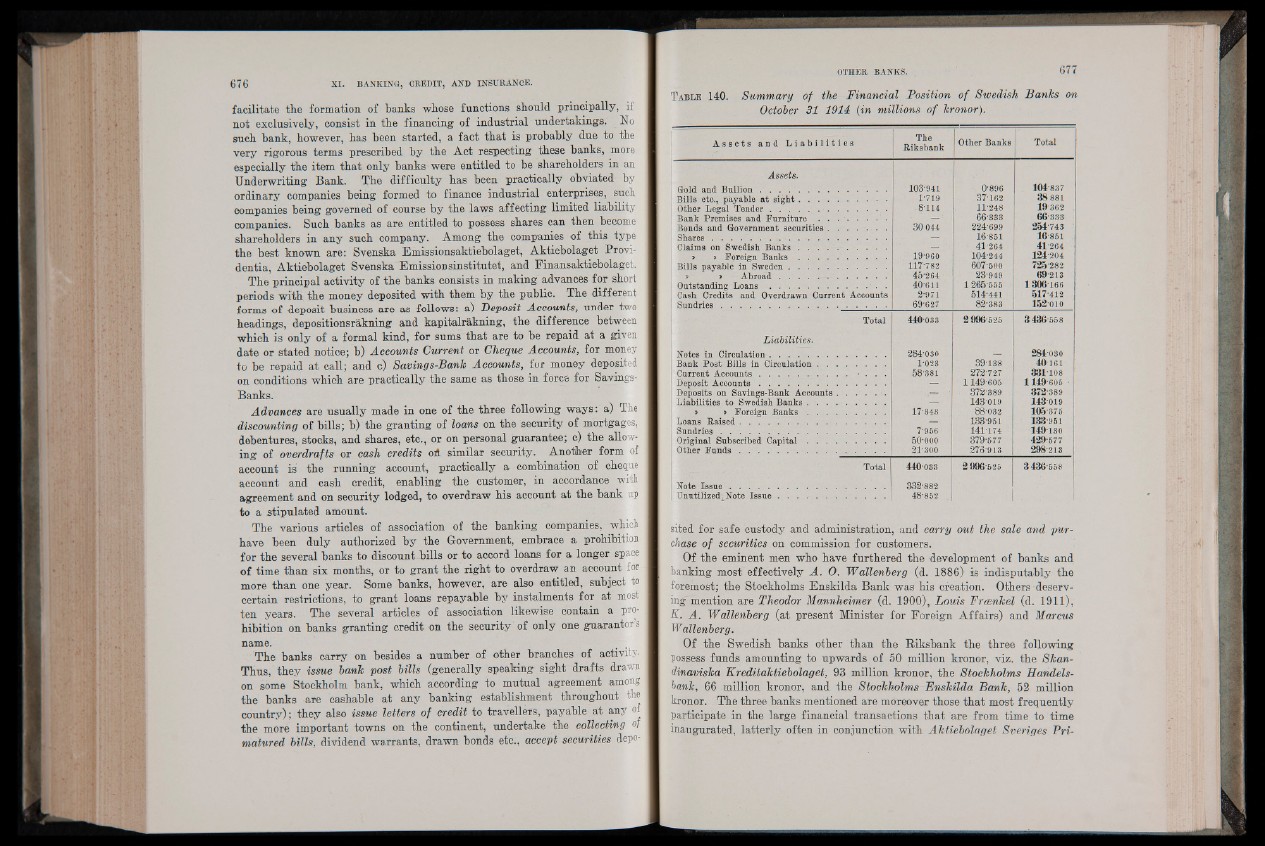

Table 140. Summary of the Financial Position of Swedish Banks on

October 31 1914 (in millions of kronor).

A s s e t s a n d L i a b i l i t i e s The

Riksbank Other Banks Total

Assets.

GMd and B u llio n ....................................................

Bills etc., payable at s ig h t....................................

Other Legal T en d e r...............................................

Bank Premises and Furniture ............................

Bonds and Government securities........................

S h a re s ........................................................................

Claims on Swedish B a n k s ....................................

> > Foreign B a n k s ....................................

Bills payable in Sweden........................................

> > A b ro a d ...........................................

Outstanding L o a n s ........................................... .

Cash Credits and Overdrawn Current Accounts

103-941

1-719

■ 8-114

30 044

" 19-960

117-782

45-264

40-611

2-971

69-627

0-896

37-162

11-248

66-333

224-699

16-851

41-264

‘104-244

607-500

23-949

1265*555 -

514-441

82-383

104-837

38 881

19362 .

66-333

254-743 '

16-851 .

41-264

124-204

725-282

69-213

1306-166

517-412

152-010

Total 440-083 2996-525 3 436 558

Liabilities.

Notes in Circulation........................................

Bank Post-Bills in Circulation............................

Current Accounts............................... . . . . .

Deposit A c co u n ts............................................

Deposits on Savings-Bank Accounts...................

Liabilities to Swedish Banks................................

> > Foreign B a n k s ................................

Loans Raised...........................................................

Sundries ....................................................................

Original Subscribed C a p it a l ................................

Other F u n d s ....................... ...................................

284-080

1-023

58-381

17-343

7-966 ■ -

50 000

21-300

39-138

272-727

1149-605

372-389

143019

88-032

133-951

141-174

379-577

275-913

284-030

40 161

331-108

1149-605 •

372-389

143 019

105-375

133951

149-130

429-577

298-213

Total 440 033 2996-525 3436-558

Note I s s u e ................................................................

Unutilized, Note I s s u e ............................................

332-882

48-852 ;.'j

sited for safe custody and administration, and carry out the sale and purchase

of securities on commission for customers.

Of the eminent men who have furthered the development of banks and

banking most effectively A. 0 . Wallenberg (d. 1886) is indisputably the

foremost; the Stockholms Enskilda Bank was his creation. Others deserving'

mention are Theodor Mannheimer (d. 1900), Louis Froenkel (d. 1911),

K. A. Wallenberg (at present Minister for Foreign Affairs) and Marcus

W allenberg.

Of the Swedish banks other than the Riksbank the three following

possess funds amounting to upwards of 50 million kronor, viz. the Skan-

dinaviska Kreditaktiebolaget, 93 million kronor, the Stockholms Handels-

bank, 66 million kronor, and the Stockholms Enskilda Bank, 52 million

kronor. The three banks mentioned are moreover those that most frequently

participate in the large financial transactions that are from time to time

inaugurated, latterly often in conjunction with Aktiebolaget Sveriges Pri